Section outline

-

Personal Budgeting

-

-

The 50/30/20 Model

The 50/30/20 model is a straightforward and practical approach to budgeting that helps you allocate your income effectively.

By dividing your income into three categories: 50% for needs, 30% for wants, and 20% for savings, you can ensure that your essential expenses are covered, enjoy some discretionary spending, and still save for the future.

The model is useful because it promotes financial balance and helps you build a secure financial foundation.

Select a segment from the pie chart below, to reveal what’s included in each category.

Now that you’re familiar with the model, it’s time to put it into practice. In the activity below, identify which expenses fall into the category of wants, needs and savings:

Take a moment to reflect on your recent purchases. Can you identify which ones were needs, which were wants, and where you might find opportunities for savings? Recognising these distinctions can help you make more informed financial decisions.

When you’re ready, move on to the next Sprint.

-

Income and Expenditure

Recognising what’s coming in and what’s going out is really important for effective financial management. This Sprint will support you in identifying all your sources of income and track your expenses too.

Income and expenses can change month to month, and we will explore ways to manage this in a later Sprint. But for now, try to gain a clear picture of your financial situation by completing the income and expenses tool below. Please note, no data is stored on this.

Income and expenses can change month to month, and we will explore ways to manage this in a later Sprint. But for now, try to gain a clear picture of your financial situation by visiting the Money Helper budget planner. This is a government backed website, and is safe to use.

Reflecting on Your Income and Expenses

Take a moment to reflect on what you’ve learned about your income and expenses. Ask yourself the following questions to gain deeper insights into your financial habits and identify areas for improvement.

- What surprised you the most about your income and expenses?

- Reflect on any unexpected findings. Did you realise you have more or less income than you thought? Were there any expenses you didn’t account for? Consider how these findings align with the 50/30/20 model.

- What changes can you make to improve your financial situation?

- Think about practical steps you can take to manage your money better. For example, can you reduce spending on wants (30%) to free up more money for needs (50%) and savings (20%)?

- How do you feel about your current financial habits?

- Reflect on your spending and saving habits. Are you happy with how you manage your money, or do you see room for improvement? How well do your habits align with the 50/30/20 model?

- How can the Financial Literacy Toolkit support you in achieving these goals?

- Identify the resources and strategies within the toolkit that can help you reach your financial goals. This might include budgeting tools, tips for saving money, or advice on managing debt. Consider how these resources can help you better apply the 50/30/20 model to your finances.

- What surprised you the most about your income and expenses?

-

Introducing Zero Based Budgeting (ZBB)

In this Sprint, you’ll learn how to plan for the month ahead using the Zero-Based Budgeting (ZBB) approach. By now, you should have a general idea about your income and expenses, but things can change from month to month, and it’s important to plan for this. The ZBB approach starts from zero each month and requiring you to justify every expense for the month ahead. By building on your existing knowledge, ZBB ensures your budget remains flexible and adapts to any changes, helping you stay on track financially.

4 Steps to ZBB

So, what does ZBB involve? Select the four steps below to reveal more.

1. List Your Income

Record all sources of income for the upcoming month.

Why: Knowing how much money you have coming in is the foundation of your budget.

How: Include all sources such as wages, allowances, student finance, or any other income. Write down the expected amount from each source.

2. Identify Expenses

List and justify all expenses, ensuring each one is necessary.

Why: Recognising where your money goes helps you manage it better.

How: List all your expenses and categorise them into needs, wants, and savings/debt repayment.

3. Allocate Funds

Ensure your total expenses match your total income, giving every pound a purpose.

Assign specific amounts to each expense category based on these percentages. Adjust if necessary to ensure your total expenses do not exceed your total income.

Why: This ensures you live within your means and avoid debt.

How:

50% Needs: Remember, these are essential expenses you can’t avoid, such as rent, utilities, groceries, and transport.

30% Wants: Non-essential expenses that enhance your lifestyle, like dining out, entertainment, and hobbies.

20% Savings and Debt Repayment: Savings, investments, and paying off any debts.

4. Monitor and Adjust

Keep an eye on your spending throughout the month and adjust to stay on track.

Compare your actual spending with your budget regularly. Check if your spending aligns with the 50/30/20 model. If you overspend in one category, try to cut back in another to stay within your overall budget.

Why: Regular monitoring helps you stick to your budget and make necessary adjustments.

How: Keep a record of all your expenditures.

ZBB in Practice

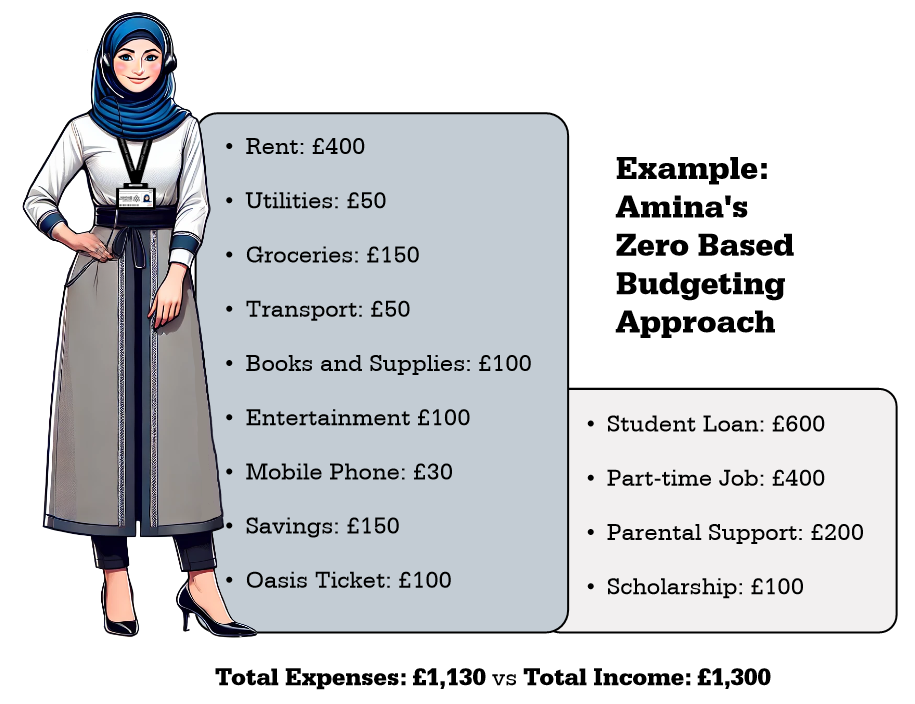

So what does this look like in practice? Have a look at the example to see how Amina’s budget may change from month to month and how ZBB helps manage those fluctuations. When you are ready, download the ZBB planner below for future use.

Amina ensures that her total expenses (£1,130) do not exceed her income (£1,300). Throughout the month, she tracks spending and adjusts her budget as needed. For example, if she spends less on groceries, she can allocate extra funds to her wants or savings and stay closer to the 50/30/20 model.

To get started, download our offline budget tracker below, and continue with the Sprint where you’ll find further guidance and examples to support you in using the planner.

Experiencing a budget shortfall is not uncommon during student life. However, it’s important to manage this effectively. The Financial Literacy Toolkit can guide you in managing your finances more efficiently. Utilise the resources and strategies offered to help you balance your budget.

Reassurance and Next Steps

Remember, it’s common to find yourself in a deficit, especially as a student. The Financial Literacy Toolkit is here to help you manage your finances better. Explore the resources and strategies provided to find ways to balance your budget.

Well done on completing topic (sprint) 1 on personal budgeting. The next topic will look at financial products.’

-