Section outline

-

Financial Products

-

-

Students mustMark as done

Common Financial Terms

As a student, managing your finances is an essential part of daily life.

Financial products are tools and services provided by financial institutions to help you manage your money. This section introduces the financial products you’re most likely to encounter. Some products may be more familiar to you than others, but each is described with its key features and benefits, helping you recognise their importance, analyse their functions, and apply this knowledge to your financial decisions. There are 10 products to explore; use the arrows below to navigate the carousel.

Financial Products Quiz

Ready to test your knowledge? Identify the best product for Alex's needs:

Reflecting on Financial Products

As you embark on your journey as a student, the financial products you choose will play a crucial role in shaping your financial well-being. From student loans to savings accounts, each product offers unique features and benefits designed to support your needs.Take a moment to reflect on the financial products we’ve explored. How might these tools help you manage your money more effectively? Consider the importance of identifying the right products for your circumstances and needs. Making informed decisions about which financial tools to use can significantly impact your financial future.

In the next Sprint, we’ll delve into the dilemma of Savings vs Borrowing. You’ll learn about the pros and cons of different financial strategies and how to make confident decisions with your money. Your journey to financial literacy continues here.

-

Saving vs Borrowing

As a student, you will have to make decisions that impact you financially. For example, imagine your laptop has broken and needs replacing. When faced with an expensive purchase like this, you have two choices: borrowing or saving.

Borrowing money is a serious commitment, and you need to ensure you can repay it to avoid potential issues down the line. Saving takes longer, but it allows you to buy what you want outright without any future repayments. Should you use credit or dip into savings?

Use the flowchart below to help you decide whether to borrow or save. 5 coins to the left = borrow; 1 coin to the right = save! (Please note, it’s normal to find that the flow chart suggests you save before making a purchase).

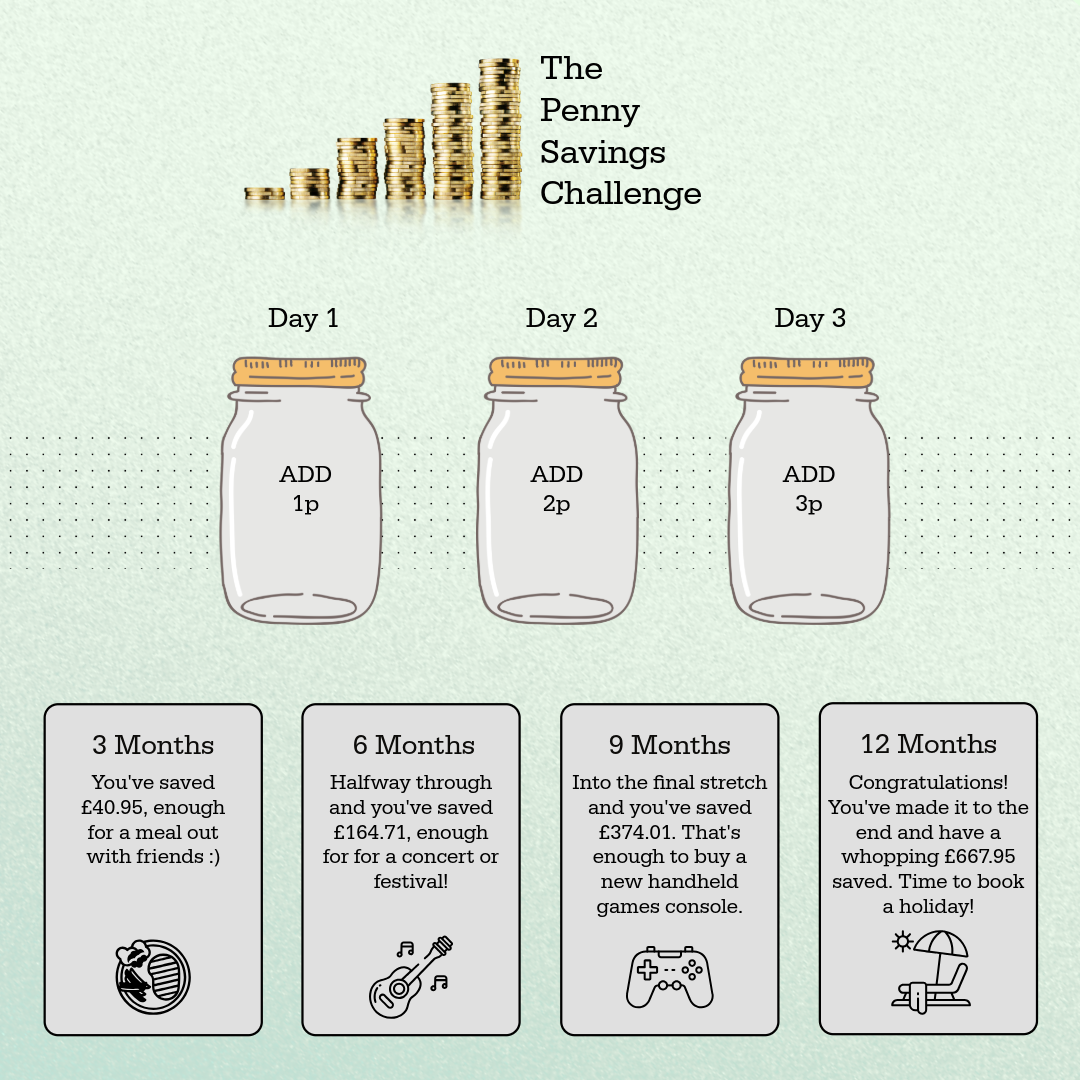

The Penny Savings Challenge

The penny saving challenge is a money saving method that lasts 365 days. It works by increasing the amount you save by 1p each day of the year.

On the first day of the challenge, you start by saving one penny. This rises to two pennies on the second day, three pennies on the third, four pennies on the fourth, and so on.

On the last day of the year, which is the 365th day, that amount rises to £3.65. Once combined, all of these smaller amounts add up to £667.95.

The challenge can make saving feel manageable and achievable alongside your studies. It’s a low-effort way to start putting money aside for something meaningful without needing to make major changes to your budget.

-

Students mustMark as done

Financial Health

Credit Scores

What is a credit score? Essentially, it’s your financial reputation. Even if you’re not currently planning to buy a house or take out a loan, your actions today – like paying your phone bill – can influence your future opportunities. It acts as a numerical representation of your creditworthiness, playing a crucial role in your financial life. The higher your score, the better your credit rating.

Why does it matter?

Your credit score matters for several reasons:

Determining Loan Approval

Lenders use your credit score to decide whether to approve you for a variety of different loans. A higher score increases your chances of approval.

Affects Interest Rates

Your credit score can qualify you for lower interest rates, saving you money over time. A poor score might mean higher rates or even being denied credit.

Renting a Home

Landlords often check credit scores to assess if you’re likely to pay rent on time. A low score might require a larger deposit or a co-signer.

Utility and Mobile Contracts

Utility companies and mobile providers may check your score. A low score could mean paying a deposit upfront being required.

Employment Opportunities

Some employers (especially in finance) may check your credit report as part of the hiring process to gauge responsibility.

Insurance Premiums

In some countries, insurers use credit scores to help determine car or home insurance premiums.

Financial Flexibility

A strong credit score gives you more options and better terms when you need to borrow or make big purchases.

Your Credit Report

Regularly checking your report is really important for staying on top of your credit, ensuring your information is accurately reported to credit bureaus, and identifying any fraudulent activity.

First, explore the interactive dashboard below to see what makes up Alex’s report. Click on the ‘i’ icons to reveal more details about the various factors that influence your credit score.

In the UK, there are several credit reference agencies (CRAs) that keep track of your credit report. These agencies collect and maintain information about your credit history, which is used to calculate your credit score. By law, all CRAs must provide you with a free copy of your statutory credit report. You can check your credit report as often as you like, and it won’t affect your score. It’s worth getting a copy of your credit report from all CRAs if you haven’t applied for it before or if you haven’t checked it for some time. This is because they might have different information from different credit providers, although there is quite a lot of overlap between them.

Accessing Your Credit Report (Activity):

Task 1: Access your credit report from at least one of the CRAs listed below. These four CRAs are recommended by MoneyHelper.org.uk, a government website. While Manchester Met does not endorse any specific CRA, customer review links are provided below to help you make an informed decision:

Task 2: Review the information in your credit report. Look for any discrepancies or errors.

Task 3: Note any areas that need attention or improvement.

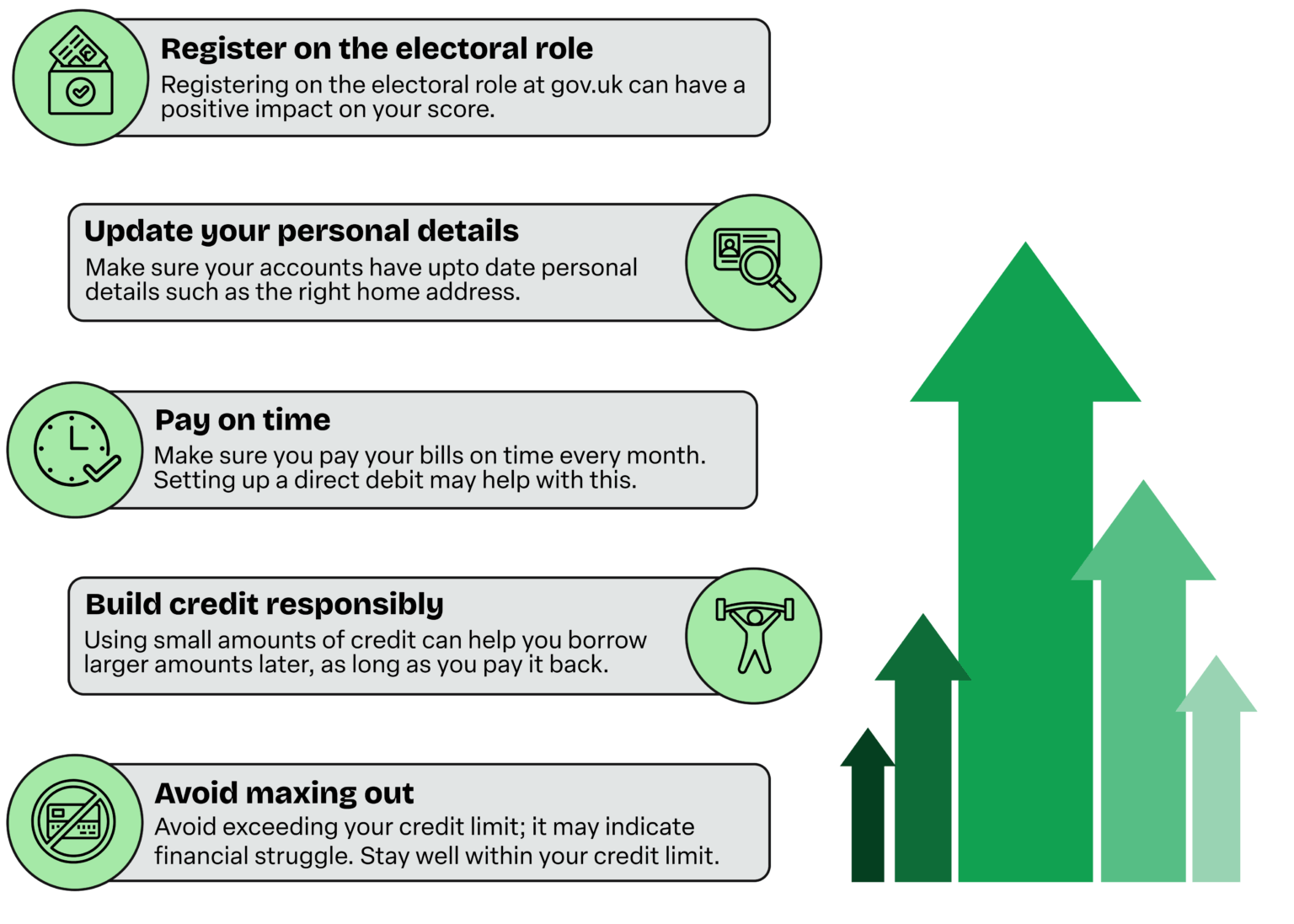

Task 4: If your credit score is low or needs improvement, check out the infographic below. It outlines five simple steps to enhance your credit score. From registering on the electoral roll to managing credit responsibly, each step helps build a stronger financial profile over time.

Silver blue header

Take some time to reflect on what you found in your credit report. Consider how you can maintain or improve your credit score based on the information in your report.

-