Section outline

-

Money and Me

-

-

Students mustMark as done

Student Loans

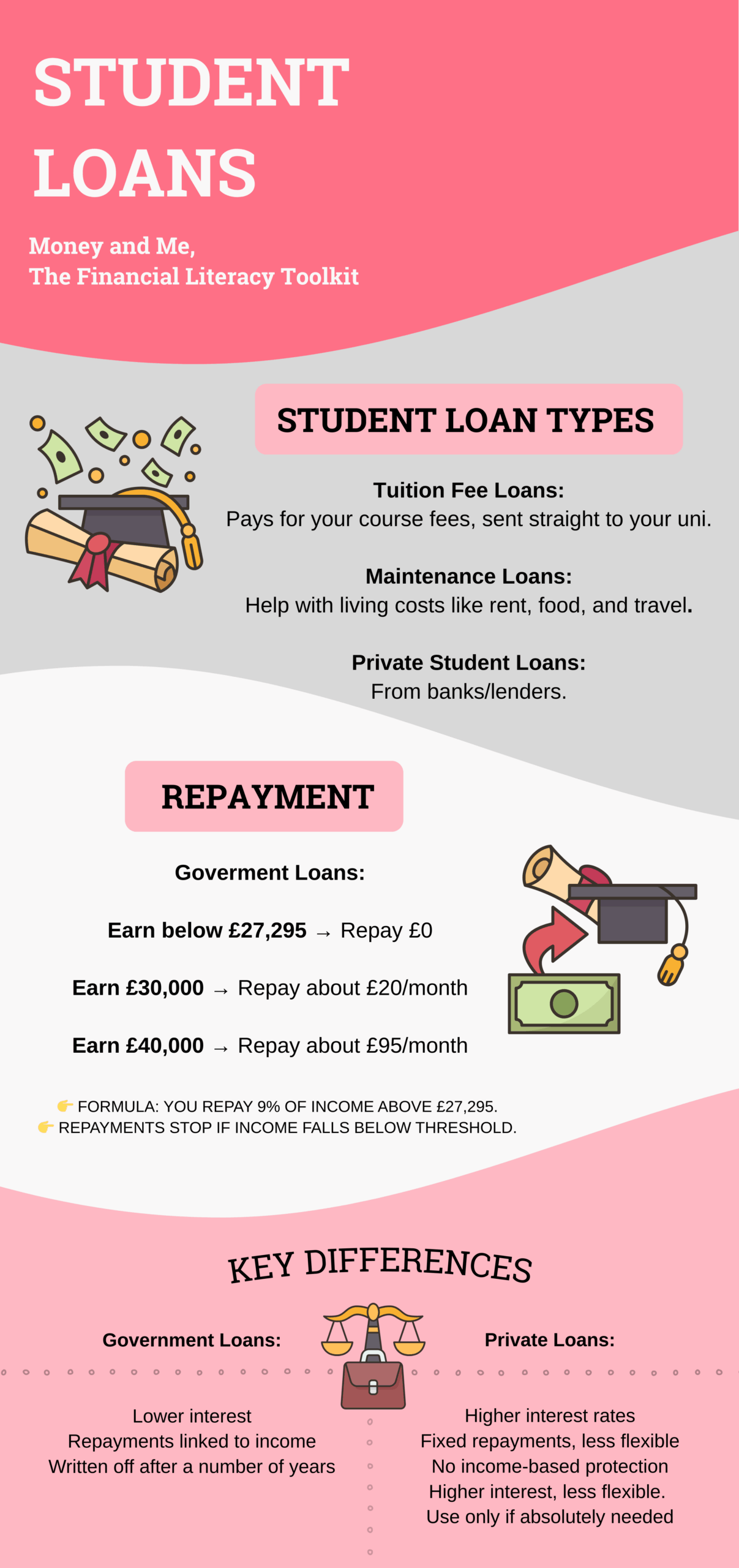

Student Loans: Getting to Grips with the Basics

Starting university often means, for the first time, needing financial support to cover tuition fees and living costs. Most undergraduates in the UK use student loans to help make university affordable.

But “student loans” can feel confusing – different types, repayment rules, and myths about debt can make it seem more complicated than it really is.

The infographic below breaks down:

- The main types of student loans you may encounter.

- How repayments actually work once you graduate.

- The key differences between government-backed and private loans.

What This Means for You

If you’re studying as an undergraduate in England, the loans you are most likely to use are:

- Tuition Fee Loans – covering your course fees.

- Maintenance Loans – supporting your living costs.

Repayments are not immediate. You only start paying back once your income is above £27,295, and what you repay depends on your earnings, not on the size of your loan. For most students, this means smaller monthly payments at the beginning of their careers, with repayments increasing only if income rises.

Any remaining balance is written off after 40 years, so the system is designed to adjust to your circumstances over time.

Private loans are available, but they usually come with higher interest and stricter repayment terms, so they’re best avoided unless there are no other options.

Your Payslip

If you decide to take paid employment while studying, understanding your payslip will give you an awareness of what has been deducted, and what remains as your take home pay. While payslips differ from one organisation to the next, they all provide the same key information. Click on the highlighted areas of the example payslip below to learn how your monthly salary is broken down, including what’s added and what’s deducted, before you receive your take-home pay.

Reflection ActivityTake a few minutes to think about your own situation:

- Which type(s) of loan are most relevant to you right now?

- How do the repayment examples (£0 at £25k, £20 at £30k, £95 at £40k) change the way you think about borrowing?

- If you had to explain student loan repayments to a friend, what’s the one key fact you would highlight from this infographic?

-

Introduction to Tax

As you step into the world of work – whether through part-time jobs, internships, freelance gigs, or graduate roles – tax becomes a part of your financial reality. But tax isn’t just about deductions; it’s a system that helps fund public services like healthcare, education, and infrastructure. Understanding how it works empowers you to manage your money more confidently and make informed decisions.

In this section, we’ll break down the main types of tax you’re likely to encounter as a student or recent graduate. Some may already apply to you, while others will become relevant as your career progresses.

Use the dropdown below to explore each type of tax and how it affects your income.

Income Tax

- Paid on money you earn from employment.

- Everyone has a Personal Allowance (£12,570) that they can earn before paying any income tax.

- Income above this threshold is taxed in bands (20%, 40%, 45%).

- Example: If you earn £25,000, only the amount above £12,570 is taxed at 20%.

Find out more about Income Tax (GOV.UK)

National Insurance (NI)

- Paid by employees and employers once earnings are above £242 a week (about £12,570 per year).

- Funds state benefits such as pensions, maternity allowance, and jobseeker’s allowance.

- Employees pay a percentage of their salary, depending on how much they earn.

National Insurance explained (GOV.UK)

Council Tax

Landlords often check credit scores to assess if you’re likely to pay rent on time. A low score might require a larger deposit or a co-signer.

- A local tax set by councils, based on the property you live in.

- Students in full-time education are normally exempt, but you may come across it when renting outside student accommodation.

Council Tax: who has to pay (GOV.UK)

Value Added (VAT)

- A tax on goods and services, usually 20%

- It’s already included in the price of most everyday purchases, so you rarely pay it separately.

VAT rates (GOV.UK)

A Window Into Your Earnings

Once you start earning, your payslip becomes a key tool for understanding your income. It shows what you’ve earned and what’s been deducted – including Income Tax, National Insurance, Student Loan repayments, and Pension contributions.

Click through the interactive payslip to explore each section below. You’ll see how your gross pay is calculated, what deductions are made, and how your net pay (the amount you actually receive) is determined.

This activity will help you:

- Recognise the impact of these deductions on your take-home pay

- Identify key components of a payslip

- Explore how tax and other deductions are calculated

Next Steps

Consider how this knowledge might influence your budgeting, saving, or career planning. Financial literacy is a lifelong skill and making sense of tax is a powerful first step.

-

Introduction: What Are Pensions?

When you graduate and start work, retirement might feel like a lifetime away. But the financial decisions you make in your twenties and thirties can have a huge impact on your life in your sixties and beyond.

A pension is a long-term savings plan with special tax advantages, designed to give you an income when you stop working. Unlike a standard savings account, pensions often involve contributions from your employer and the government, and your money is invested to (hopefully) grow over time.

According to the Office for National Statistics, the average retirement lasts around 20 years for men and 23 years for women (ONS, 2022). That means most people need significant savings to sustain themselves after leaving work.

The main purpose of a pension is simple: to provide a replacement for your salary once you retire. Without one, you may have to rely solely on the State Pension, which in 2025/26 pays a maximum of £221.20 per week (around £11,500 per year) if you have 35 qualifying years of National Insurance contributions (Gov.uk, 2025).

Features and Benefits of Pensions

- Employer Contributions: Thanks to the UK’s auto-enrolment system, most workers are automatically enrolled into a workplace pension if they’re over 22 and earn more than £10,000 a year. Both you and your employer must contribute a minimum of 8% of your qualifying earnings (5% employee + 3% employer).

More info: Gov.uk – Workplace Pensions - Tax Relief: The government tops up your pension by refunding the income tax you would have paid on your contributions. For example, if you put in £80, the government adds £20, making £100 go into your pension. Higher-rate taxpayers get even more relief.

- Investment Growth: Pension contributions are invested in funds (e.g., stocks, bonds). Over decades, compound growth can make a huge difference — even modest contributions can grow into a significant sum.

- Locked Away Until Retirement: Pension savings are usually inaccessible until age 55 (rising to 57 in 2028), which prevents early withdrawals and encourages long-term growth.

Types of Pensions

- State Pension

- Paid by the government once you reach State Pension age (currently 66, rising to 67 and then 68).

- To qualify for the full new State Pension (£11,500 p.a. in 2025/26) you need at least 35 years of National Insurance contributions.

- Fewer years = reduced State Pension. With only 10 years of contributions, you get nothing.

- More info: Gov.uk – State Pension

- Workplace Pension

- Set up by your employer, includes contributions from both you and them.

- Your employer is legally required to contribute at least 3%.

- You can usually increase your own contributions, and many employers will match them above the minimum.

- Personal Pensions (including SIPPs)

- Arranged by individuals through banks, insurers, or online investment platforms.

- Greater flexibility and control, especially for the self-employed or those wanting to top up workplace savings.

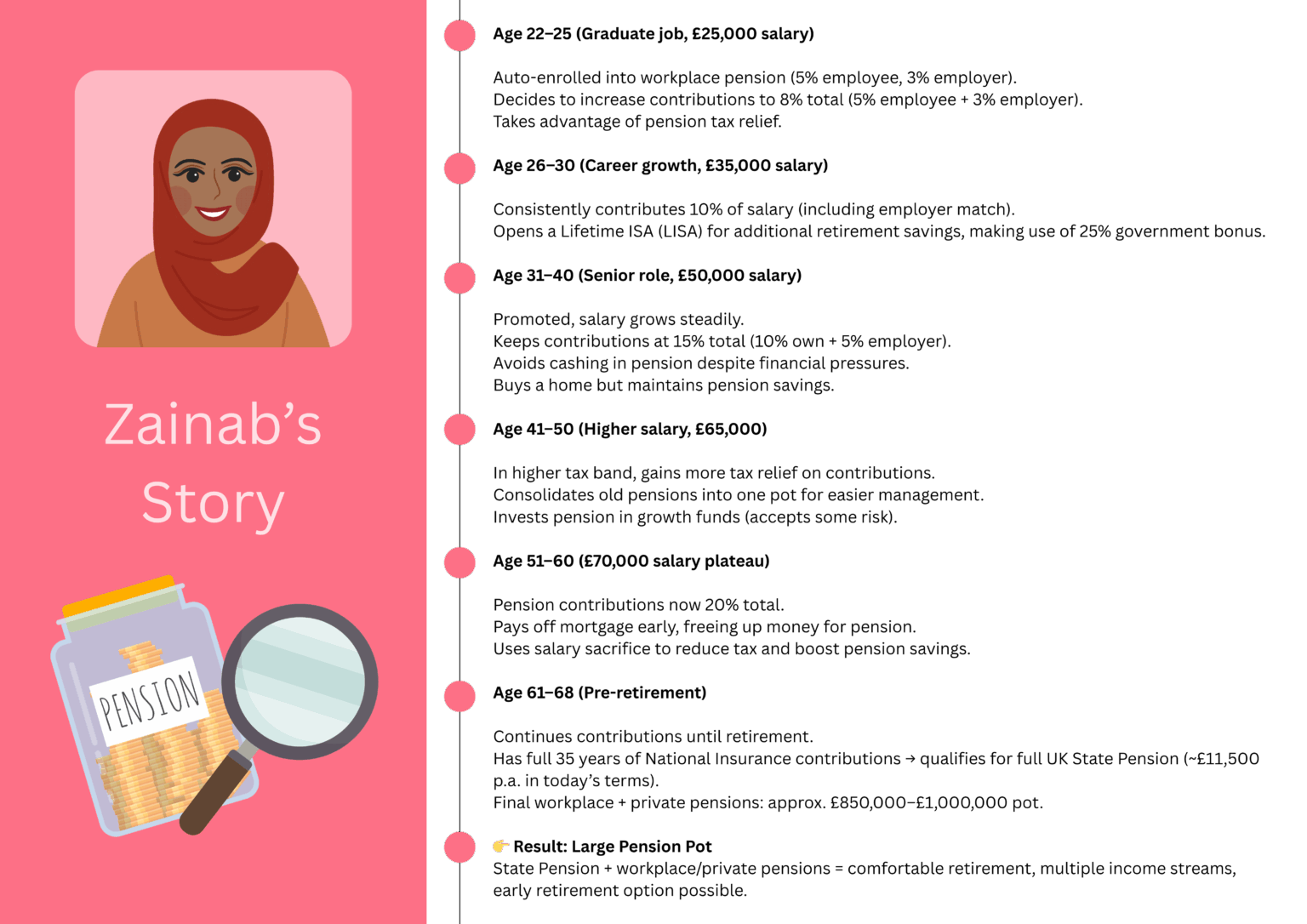

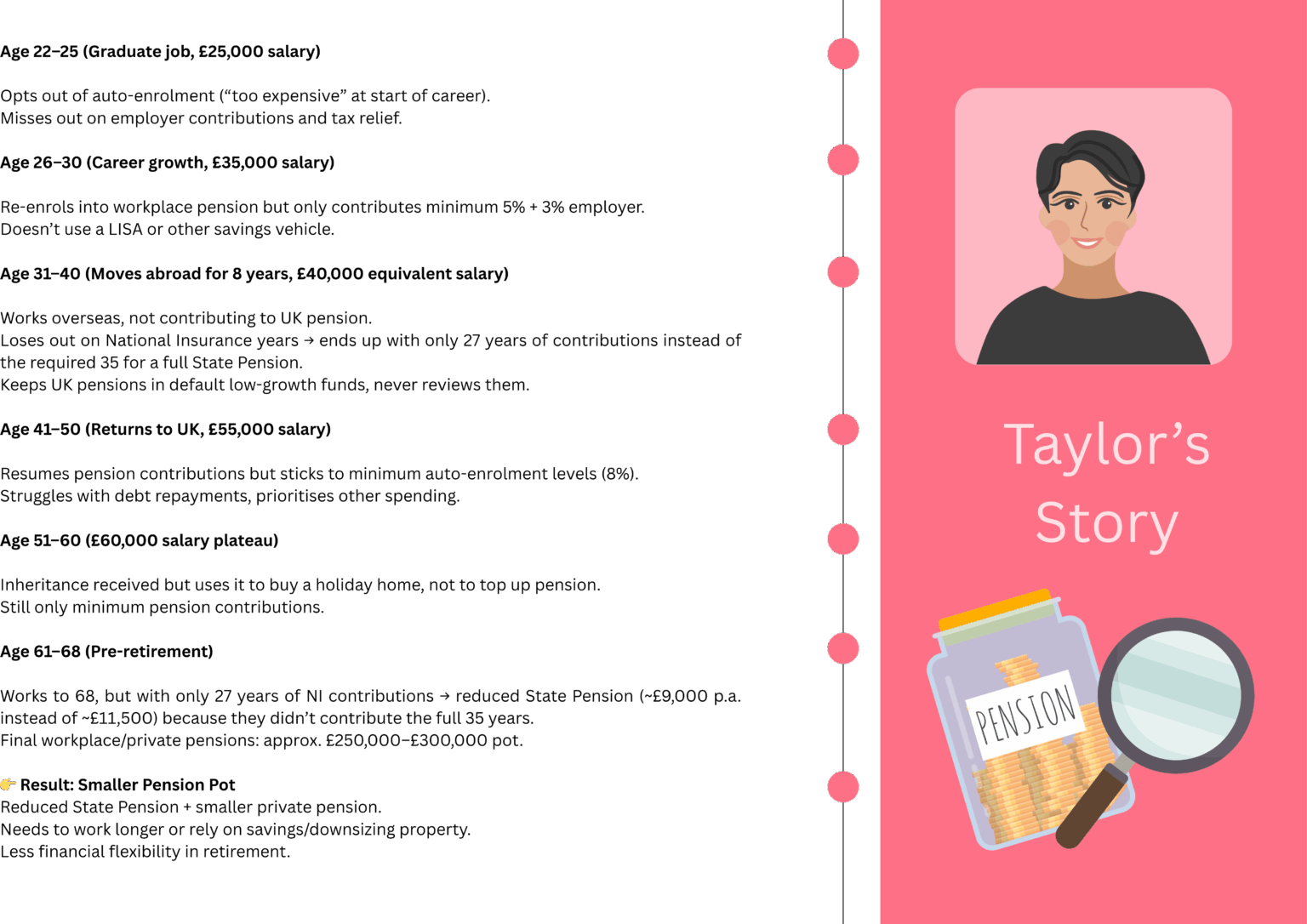

You’ve seen how pension contributions appear on your payslip, but what do they mean for your future? Let’s meet two people, Zainab and Taylor, who made different choices about their pensions throughout their working lives. Their stories show how small decisions today can shape your retirement tomorrow.

Wrap-Up & Reflection

The two stories highlight a key message: pensions are not just about the money you pay in – they’re about the long-term impact of consistent decisions.

- In Journey 1, Zainab contributed above the minimum, invested wisely, and built up a workplace pension worth nearly £1 million, plus a full State Pension.

- In Journey 2, Taylor opted out at times, contributed less, and missed out on 8 years of National Insurance, leaving them with a much smaller pension pot and only a reduced State Pension.

Key Takeaway for You as a Student:

- Even though retirement may seem far away, understanding pensions early gives you a huge advantage.

- If you know how auto-enrolment, contributions, tax relief, and National Insurance work, you can make informed choices that will pay off decades later.

Remember: the earlier you start, the more your future self will thank you.

- Employer Contributions: Thanks to the UK’s auto-enrolment system, most workers are automatically enrolled into a workplace pension if they’re over 22 and earn more than £10,000 a year. Both you and your employer must contribute a minimum of 8% of your qualifying earnings (5% employee + 3% employer).

-